Minimum Retirement Plan Distributions

Most qualified retirement plans offer significant tax benefits for those willing to follow a few IRS specified rules. The government wants to make these plans (401(k)s, Keoghs, SEPs and traditional IRAs) available for specific needs, and has established tax law to help eliminate potential abuses of these tax advantaged investment alternatives.

Retirement Plans are Intended for Retirement

For one thing, the government wants to make sure that such savings (and income tax benefits) actually go towards providing retirement income. Stiff penalties for early withdrawal help encourage investors to reserve their qualified plans for use during their retirement years.

Required Withdrawals

On the other hand, the government also wants to ensure that they will one day be able to tax these accumulated funds. If you have a 401(k), a Keogh, a SEP or a traditional IRA, you must begin taking regular distributions, or Required Minimum Distributions (RMD’s) at a certain age. If you reach 70 ½ in 2019 you must take your first RMD by April 1, 2020. If you reach 70½ in 2020 or later, you must take your first RMD by April 1 of the year after you reach 72.

Although the tax code allows you to wait until April 1 of the year following the year you turn 72 (70 ½ if you reach 70 ½ before January 1, 2020), it is generally a good idea to take your first mandatory withdrawal in the same year you turn 72. If you wait, you will have to make two withdrawals in the first year, doubling the amount of taxable income you must declare and potentially increasing your marginal tax bracket.

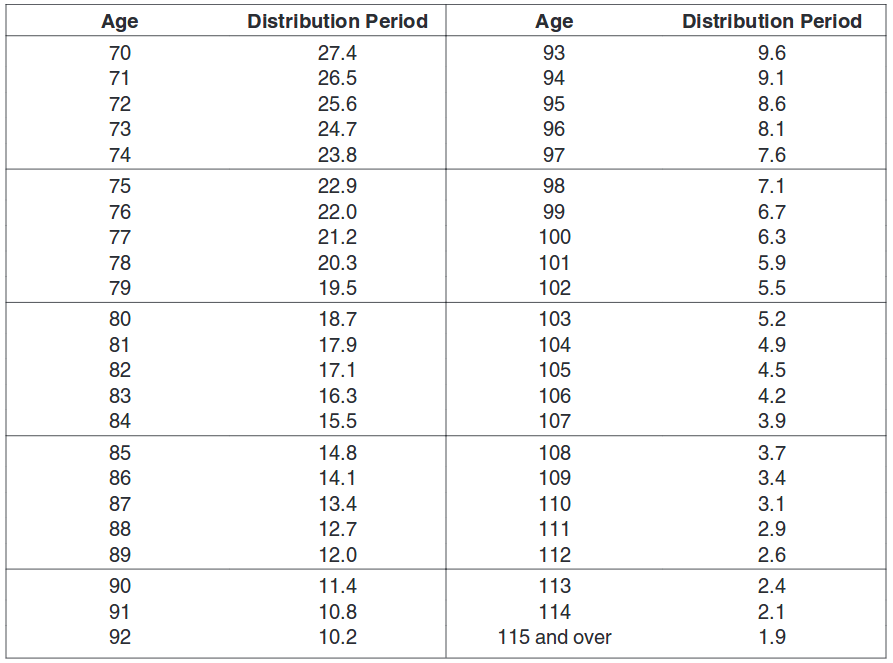

The amount you are actually required to withdraw each year, and which will be subject to taxation, is based on tables which estimate your remaining lifetime.

Calculating Your Required Withdrawals

It is very important that you maintain a structured process of minimum withdrawals from your qualified plans--if you do not meet the required minimum distribution withdrawals, the IRS will impose a penalty of 50% of the amount not withdrawn, plus the income taxes due. The good news is that the IRS has made calculating your required minimum distributions much easier than it used to be.

Based on your age, you simply divide your qualified plan balance as of the last day of the previous year by the factor from the IRS Pub. 590 table shown below. The resulting quotient is your annual required minimum distribution.

The accuracy of this record is important. You can get a copy of your earnings record from the Social Security Administration (SSA). Fill out Form 7004 and mail it to SSA. The forms are available at your local Social Security office or by calling 800-772-1213. If you discover your record is wrong, you can ask that it be corrected, though you must supply evidence of errors. The SSA encourages people to check their earnings records every three years or so, since the earlier a problem is found, the easier it is to prove and correct.

Material discussed is meant for general illustration and/or informational purposes only and it is not to be construed as tax, legal, or investment advice. Although the information has been gathered from sources believed to be reliable, please note that individual situations can vary therefore, the information should be relied upon when coordinated with individual professional advice.